SuperPay

The intelligence layer behind every transaction. AI-powered card optimization that maximizes rewards, builds credit, and transforms how people pay.

Americans leave $250B+ in rewards on the table. Every year.

The average American holds 3.8 credit cards, each with different reward structures, spending caps, and category bonuses. No one can keep track — so they default to the wrong card, every time.

No centralized intelligence

Card issuers have no incentive to help you use competitors' cards. Each app only promotes its own products.

Rewards complexity is growing

Rotating categories, quarterly caps, tiered spending thresholds, sign-up bonus requirements — it's impossible to track manually.

Zero real-time guidance at checkout

By the time you're at the register or checkout page, there's no tool telling you which card to use. You just guess.

The Intelligent Infrastructure Layer for consumer payments

One decision engine — every card, every checkout, every surface. SuperPay isn't a checkout helper; it's the routing layer that decides which card should win every transaction, worldwide. Plaid moves the data. Stripe moves the money. SuperPay decides which card to use.

Engine

AI-Powered

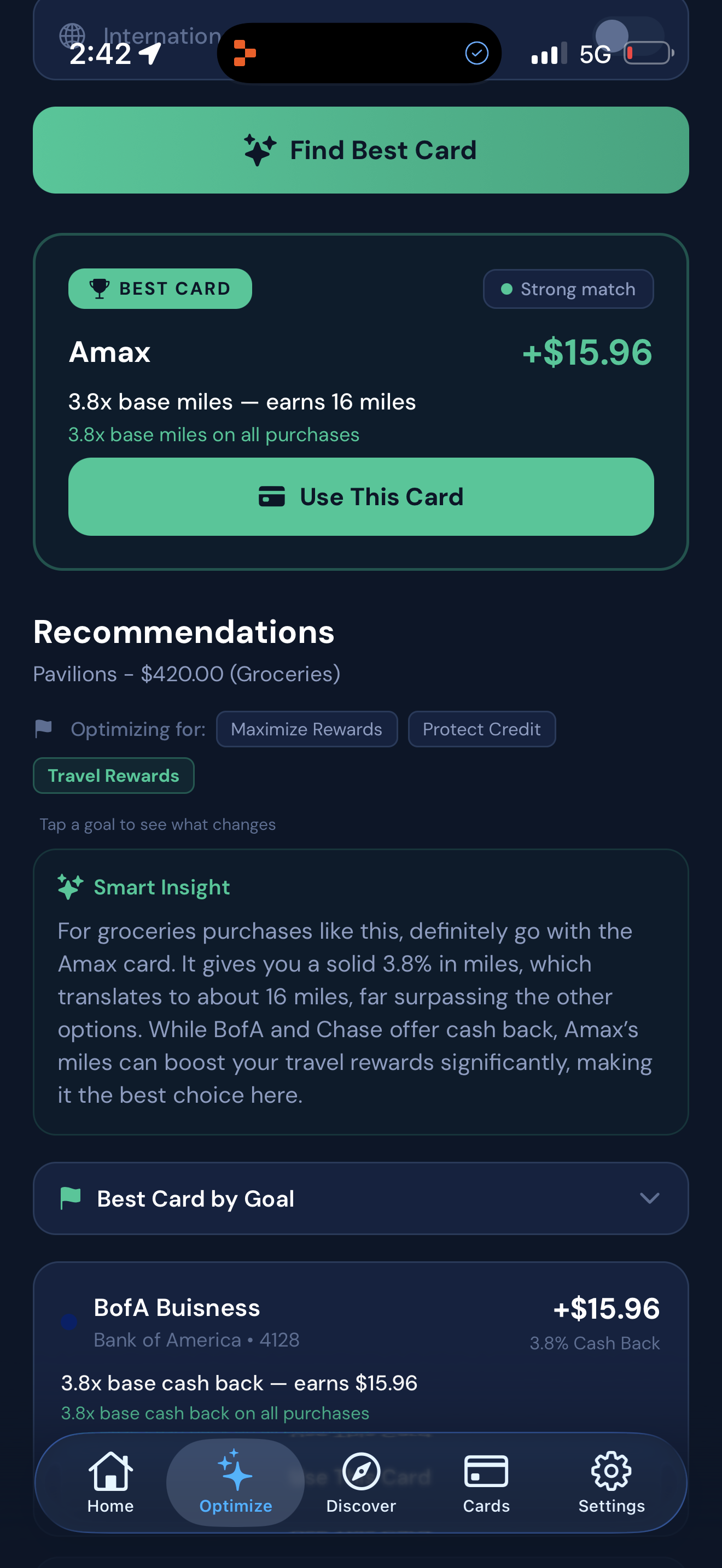

Scores every card against merchant, category bonus, and spending caps — in milliseconds, at checkout.

Location-Aware

Google Places signals identify the merchant category before the user taps — so the right card is ready.

Goal-Aware

Weights every recommendation against what matters to the user — cash back, travel miles, or credit health.

History-Aware

24 months of real Plaid transaction data — scores cards against how users actually spend, not self-reported habits.

Three steps to maximize rewards every time

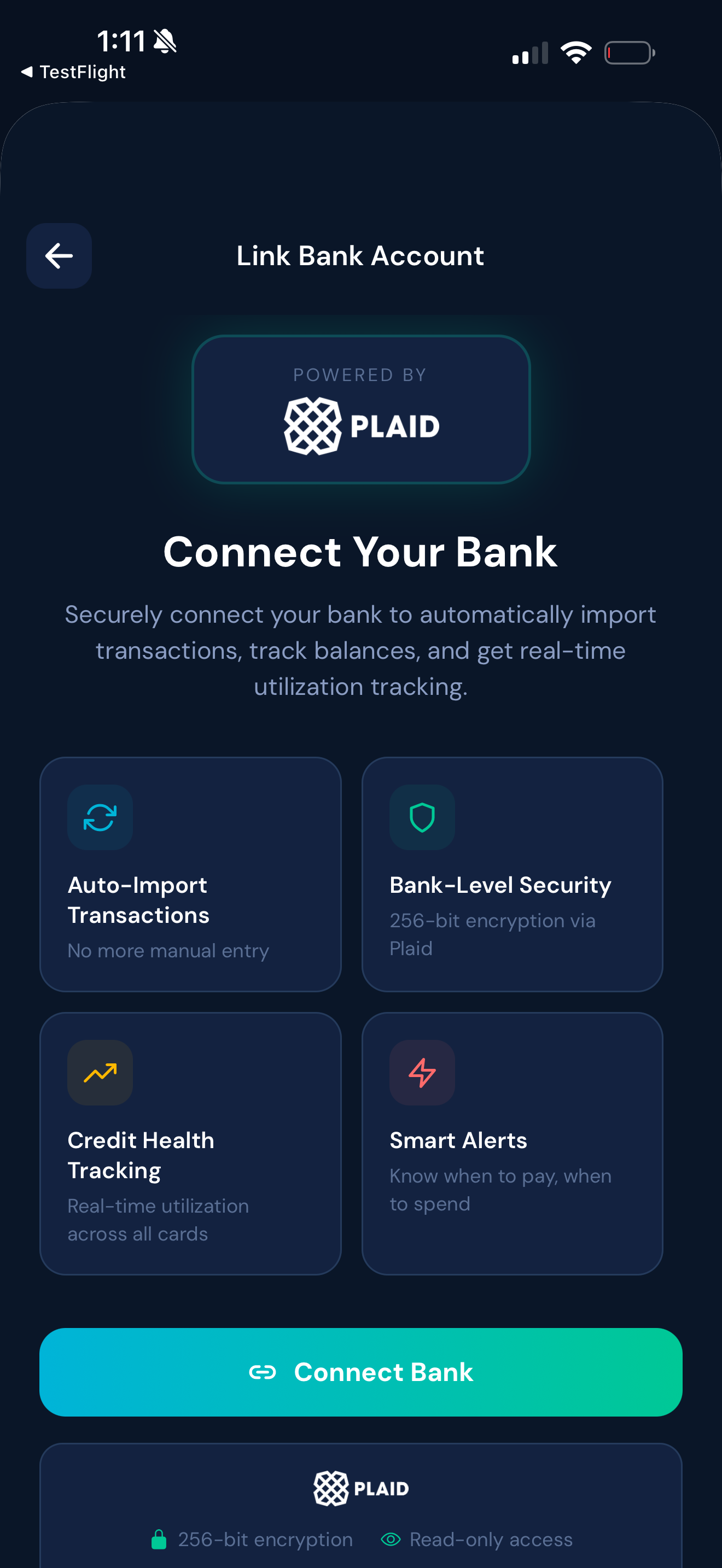

Connect your bank

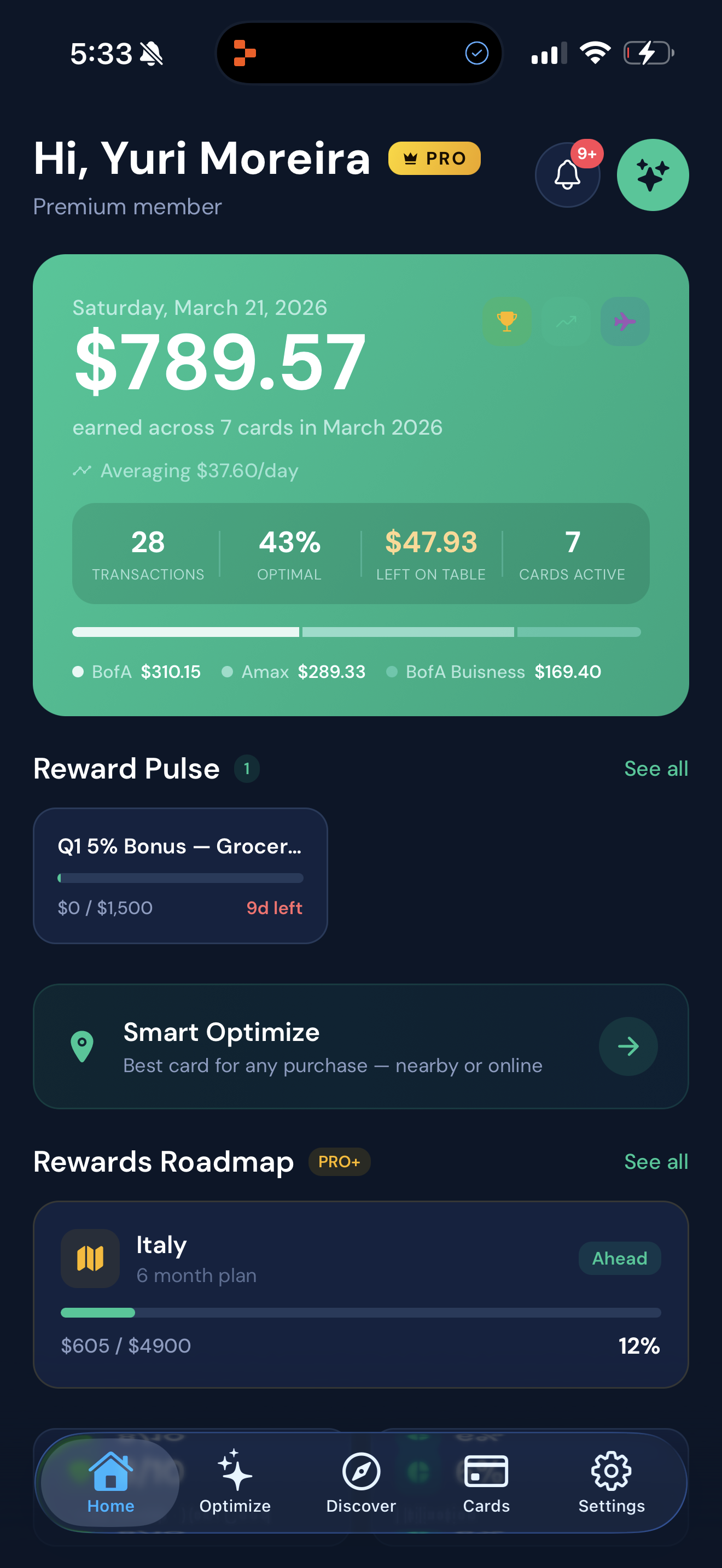

Link your accounts via Plaid in seconds. SuperPay automatically imports all your credit and debit cards with full reward structures — and analyzes up to 24 months of transaction history to show exactly how much you've been leaving on the table. No manual entry required. (Or add cards individually from our 316-card proprietary database.)

Set your goals

Choose what matters most: maximize cash back, earn travel miles, protect credit health, hit every bonus, or stay budget-conscious. SuperPay weighs every recommendation against your priorities.

Shop smarter — everywhere

Get the best card recommendation at every checkout. In-store via the mobile app, online via our browser extension, or through 80+ pre-mapped retailers. AI explains why each card wins.

A complete intelligence ecosystem

SuperPay meets users wherever they transact — mobile, desktop, and soon, directly at the point of sale.

Mobile App (iOS & Android)

Full-featured wallet intelligence: card management, optimizer with location-based detection, credit health tracking, spending insights, transaction history, AI recommendations, and 24-month missed value analysis via Plaid.

Browser Extension (Chrome & Safari)

Automatic checkout detection on 80+ retailers. Shows optimal card overlay with AI explanation directly on the payment page. One-click transaction logging. Shared auth with mobile app.

SuperPay Card (Roadmap)

Digital and physical cards that auto-route every transaction to the optimal card in your wallet. The intelligence layer becomes the execution layer — no more choosing, just tap and go.

AI Explanations

GPT-4o-mini powered conversational insights that explain why each card is optimal for a purchase. Not just numbers — real context users understand and trust.

From recommendation to automatic execution

Today, SuperPay tells you which card to use. Tomorrow, our digital and physical SuperPay Cards will automatically route every transaction through the optimal card in your wallet — in real time, at every terminal and checkout. One card to rule them all. The user just taps. SuperPay's AI handles the rest: maximizing rewards, protecting credit health, and achieving financial goals on every single purchase. This is the endgame — not just intelligence, but autonomous financial optimization.

A $4.5 trillion transaction layer

SuperPay sits at the intersection of credit card spending, fintech wallets, and AI — three massive, converging markets.

Why Now

Credit card rewards complexity is at an all-time high. AI capabilities have matured to process real-time financial optimization. Browser extension APIs enable at-checkout intelligence. Consumers are actively seeking tools to manage multi-card wallets.

Market Tailwinds

Credit card issuance growing 5% YoY. Average rewards per card increasing. Gen Z holds 2.5 cards by age 25 (vs 1.5 a decade ago). Embedded finance and digital wallets normalizing AI-assisted payments.

Freemium today. Platform revenue tomorrow.

Free Tier

3 cards, 1 goal, 2 bank connections. Full optimizer access. Enough to prove value and drive conversion. Designed as an acquisition engine.

Pro Tier — $9.99/mo

Unlimited cards & goals. Advanced insights, spending patterns, AI explanations, credit builder, 24-month analysis. Annual: $99 · Lifetime: $199

Pro+ Tier — $19.99/mo

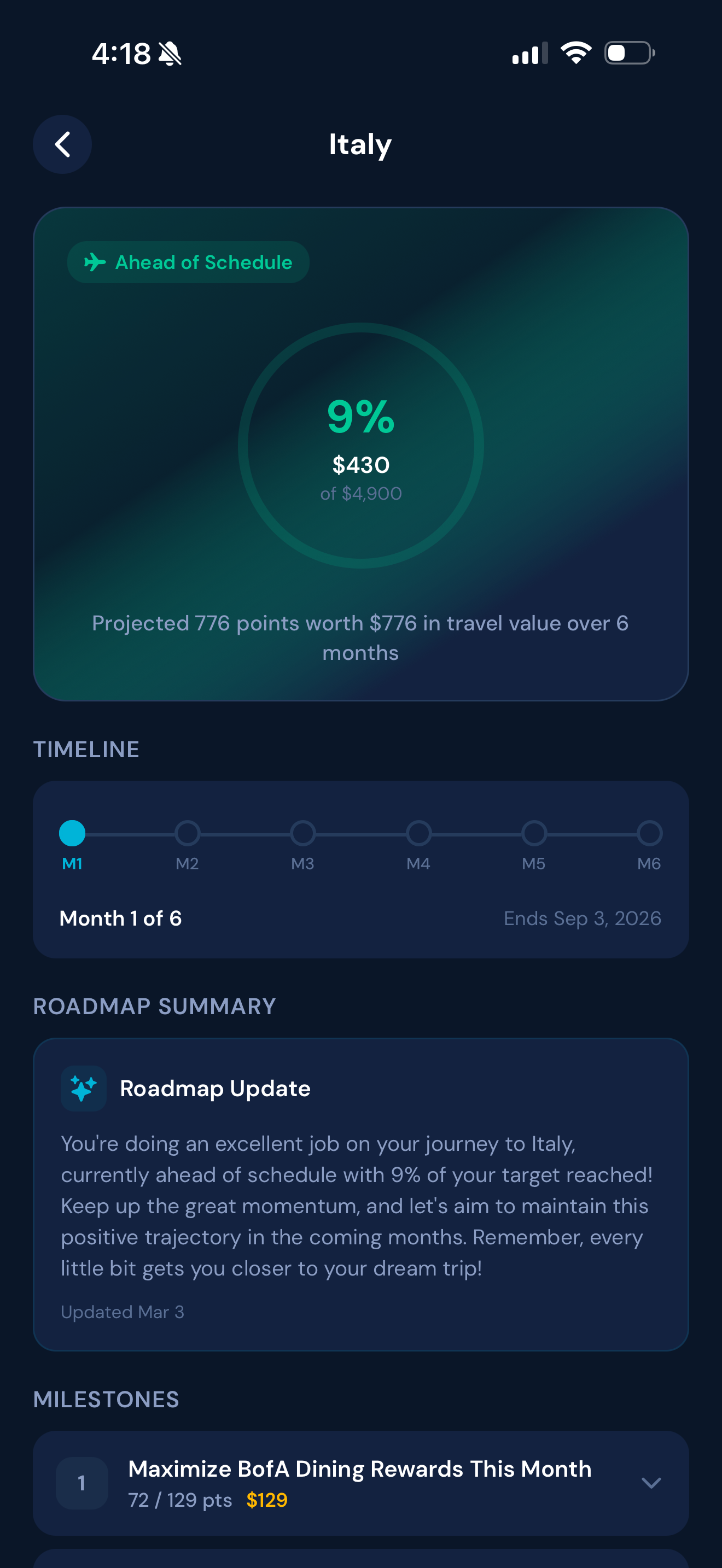

All Pro features plus the full AI Rewards Roadmap Engine: AI-generated personalized milestone titles and strategy plans, month-by-month action plans, smart new card recommendations from 316 hand-curated market cards with welcome bonus analysis, auto-detect best points ecosystem (Chase UR, Amex MR, Capital One Miles), hidden card perk discovery with goal-specific tips, and progress tracking with AI-powered insights. The premium tier for outcome-driven users.

Outcome Engineering: From Transactions to Goals

Users define a financial goal (e.g., "London trip in 6 months") and the AI Roadmap Engine builds the path to get there:

Goal-Based Projections

Projects point accumulation from your real spending patterns

AI Action Plans

Personalized month-by-month milestones unique to each user's goals

316 Cards, 12K+ Banks

Cross-references spending from 12K+ connected banks against 316 hand-curated card products

Ecosystem Detection

Auto-picks your best points currency — Chase UR, Amex MR, Capital One Miles

Hidden Perk Discovery

Surfaces unused card benefits with goal-specific contextual tips

Adaptive Tracking

AI-powered progress insights with real-time recalibration

The moat: no competitor combines real-time spending data, market-wide card intelligence, perk discovery, and goal-level AI roadmapping into a single engine.

Card Referral Affiliates

SuperPay sees every user's spending patterns. We can recommend new cards that would earn them more — and earn $50-$200 per approved referral from issuers.

Merchant Partnerships

Location-based "featured merchant" placements. Merchants pay to be highlighted in the Near You section with special offers.

SuperPay Card Interchange

When SuperPay issues its own card, we earn interchange revenue (1.5-3%) on every auto-routed transaction. This is the long-term platform play.

Bank Partner API LIVE

The same rewards engine white-labeled for financial institutions. Banks embed real-time card recommendations in their digital banking apps — billed by tier.

Sandbox (free · testing) · Growth $299/mo · Enterprise (custom)

Minimal marginal cost — 5-min cached catalog, no AI per-call cost. Adds a direct B2B ARR line on top of consumer and merchant revenue.

A B2B SaaS layer on the same engine: $49 · $149 · $299/mo

SMBs and finance teams use the same recommendation engine to optimize business card spend, route purchases to the highest-yielding card, and surface vendor-level savings. Financial institutions embed the same intelligence directly in their digital banking apps. All sold as flat-rate SaaS — no per-transaction fees, no revenue share.

SuperPay Business — $49/mo

For owner-operators and SMBs. Up to 10 business cards, business-mode merchant categorization (vendors, software, freight, ads), monthly savings reports, and unlimited goals. Single-seat. Same optimizer the consumer app runs.

Launch: month 6 · Logo churn target: ~3%/mo · Y3 ARPA: $588

SuperPay Business Pro — $149/mo × 1.5 seats

For finance teams and multi-entity operators. Everything in Business plus AI vendor narratives, a multi-seat console, AI card advisory, anomaly alerts, and CSV/QuickBooks export. Average deployment: 1.5 seats × $149.

Launch: month 9 · Avg seats: 1.5 · Logo churn target: ~2%/mo · Y3 effective ARPA: $2,682

Bank Partner API — $299/mo Growth · Custom Enterprise

For banks and fintechs. White-labeled card reward recommendations embedded in digital banking apps via POST /v1/bank/recommend and /v1/bank/portfolio. Server-to-server, sub-100ms, no shopper PII required. Same catalog — near-zero per-call marginal cost.

Sandbox free · Growth: up to 50K calls/mo · Enterprise: unlimited + SLA · Y2 ~$36K ARR · Y3 ~$72K ARR + Enterprise custom

SMB credit-card spend is a $700B+ category we already model — and banks want this engine too

Every business card in our 320-card catalog is already scored against business categories (advertising, software, fuel, shipping, travel). The SaaS layer is a packaging change, not a new engine. Expect ~993 Business and ~267 Business Pro logos by month 36 at the cadence in the model — together a ~$1.3M Y3 ARR addition with very low marginal cost. Alongside SMB, the Bank Partner API extends the same engine to financial institutions: banks embed card recommendations in their digital apps at Growth $299/mo · Enterprise custom per institution, creating a second B2B ARR stream with near-zero additional marginal cost per call (catalog is 5-minute cached; no per-call AI cost).

Three flat-rate B2B tiers — no per-transaction fees

Y3 ARR run-rate: B2B SaaS ~$1.3M + Bank API ~$72K+

Same optimizer powers consumer + B2B + Merchant API + Bank Partner API

Free checkout API. Branded distribution flywheel. + Bank Partner API

A second business: distribution at the merchant layer. The same rewards intelligence engine, packaged as a free checkout API — 320+ cards modeled, <120ms response, free forever for merchants. Every install becomes a SuperPay-branded surface at checkout and a zero-CAC funnel back into the consumer app.

One drop-in line

Drop in /v1/widget.js or call POST /v1/recommend. Returns the top 3 cards for any cart in <120ms via top_cards[]. Test with sp_test_…, ship with sp_live_….

Free for merchants — forever

No fees. No rev share. No contract. The pitch is pure AOV lift: shoppers who see real cash-back math reach for higher-tier carts. 30-second install, never breaks checkout — a $0-cost adoption decision.

Zero-CAC consumer funnel

Every install puts the SuperPay logo at checkout — a distribution flywheel at zero CAC. Shoppers without the recommended card see a CTA into the consumer app. Modeled: ~3,600 net-new consumer signups/month from merchant installs by month 36 (~16% of channel-attributed new users in Year 3).

Why we don't charge — and where the money does come in

The API itself stays free. In Year 3 we layer an optional Merchant Analytics tier at $99/mo for merchants that want category-level conversion lift dashboards (~5% adoption modeled). The real return is consumer acquisition: every install is a permanent, branded acquisition channel. Direct API monetization shows up only in Y3; the funnel impact compounds from month 4.

The same intelligence engine, white-labeled for banks and fintechs

Financial institutions embed real-time card reward recommendations directly in their digital banking apps via two REST endpoints (POST /v1/bank/recommend and POST /v1/bank/portfolio). Server-to-server, sub-100ms, no shopper PII required. Self-serve onboarding at superpayrewards.com/for-banks.

recommend endpoint only

recommend + portfolio

full access + SLA + dedicated support

Projection: 10 Growth partners by Y2 (~$36K ARR) → 20 Growth + 3 Enterprise partners by Y3 (~$72K ARR + Enterprise custom revenue). Same catalog infrastructure as the merchant API — near-zero per-call marginal cost.

Cards modeled in the recommendation catalog

Typical response time, served from edge

Modeled cumulative merchant installs by m36

3-Year revenue evolution

A layered model that shows capital efficiency, scalable economics, and upside asymmetry.

Core Assumptions

Consumer subscription: Pro $9.99/mo · Pro+ $19.99/mo · Annual $99-$199 · Lifetime sunset at 25K

Affiliate: 5% of users annually · $150 avg payout

SuperPay Business: $49/mo (m6+) · Business Pro: $149/mo × 1.5 avg seats (m9+)

Merchant API: free forever · optional $99/mo analytics tier (Yr 3+, ~5% adoption)

Bank Partner API: Sandbox free · Growth $299/mo · Enterprise custom · Y2 ~$36K ARR · Y3 ~$72K ARR + Enterprise custom

Interchange (Yr 3+): 0.5% net share

Year 1 — Intelligence Layer Validation

| Scenario | Users | Revenue |

| Conservative | 75K | ~$1.0M |

| Base | 100K | ~$1.4M |

| Aggressive | 150K | ~$2.2M |

Focus: Paid conversion · Retention · Affiliate · Business launches m6, Business Pro m9, Merchant API installs from m4 (~$0 direct revenue, ~1% of new users)

Year 2 — Scale + Card Beta

| Scenario | Users | Revenue |

| Conservative | 300K | ~$4.0M |

| Base | 500K | ~$6.9M |

| Aggressive | 750K | ~$10M+ |

Focus: Card beta · Routing · 7-8% conv · B2B SaaS scaling (Business + Business Pro ~$0.3M ARR by Y2 end, Merchant API ~6% of new users, Bank Partner API ~$36K ARR from ~10 Growth partners)

Year 3 — Routing Infrastructure Active

| Scenario | Users | Revenue |

| Conservative | 750K | ~$20M |

| Base | 1M | ~$30M-$40M |

| Aggressive | 2M | ~$50M-$60M |

Revenue mix: Consumer Subscription + Affiliate + Interchange (dominant) + B2B SaaS ~$1.3M ARR run-rate (Business $0.6M + Business Pro $0.7M) + Bank Partner API ~$72K ARR from ~20 Growth + 3 Enterprise partners + Merchant API analytics tier ~$71K ARR run-rate (~$48K recognized Y3 revenue, ramps from m25); Merchant API funnel ~16% of channel-attributed new users

Strategic Insight

18-month raise target: 250K users · $5M+ ARR — tracking between Year 1 Aggressive and Year 2 Base.

Year 3: Interchange + B2B SaaS + Bank Partner API + Merchant API together transform SuperPay from a single-product wallet into multi-rail infrastructure (~$1.3M B2B SaaS ARR run-rate + ~$72K Bank API ARR + Enterprise custom, ~16% of channel-attributed new users via Merchant API).

Interchange Assumptions (Year 3)

Conservative: 15% card adoption · ~$10M-$15M

Base: 25% adoption · ~$20M-$25M

Aggressive: 25-30% adoption · ~$30M+

SuperPay creates a new category

We don't compete with card issuers or budgeting apps. We're the intelligence layer they all lack.

Every other tool forces the same trade — market-wide OR automatic. SuperPay is the first product that's both.

Product & Build Status

Pre-launch — public launch coming. Numbers below reflect product readiness, not user traction.

Hand-Curated

Identified

Mapped

Shipped

Product Completeness

Full iOS/Android/Web app with 5-tab navigation, guided onboarding, Plaid integration, AI explanations, browser extension, merchant checkout widget + REST API, landing page, privacy/terms/support pages, and download infrastructure — all built and functional.

Key Milestones

MVP shipped end-to-end by a solo founder; production app live on superpayrewards.com.

✓ Merchant checkout API live (320+ cards modeled, <120ms response, free for merchants, opt-in effective-cost line under the pay button)

✓ MVP app complete with full optimization engine

✓ AI-powered recommendation explanations

✓ SuperPayRewards.com live with professional presence

✓ Browser extension with checkout auto-detection (Chrome + Safari)

✓ Google Places API integration for location intelligence

✓ Up to 24 months of historical missed value analysis (PRO+)

✓ PRO+ Rewards Roadmap Engine v2

Defensible intelligence that compounds over time

Proprietary Card Database

316 cards with exact reward rates, category bonuses, and spending caps. Hand-curated and continuously updated — with access to 12,000+ cards across 12K+ banks via Plaid.

Merchant Intelligence

Any merchant with a business address — identified via Google Places API. AI-powered categorization with keyword pattern matching. 30+ Place type mappings.

Client-Side Optimizer

Goal-aware scoring runs on-device for instant recommendations. No latency, works offline, privacy-preserving.

Plaid Deep Integration

Up to 24 months of transaction history analysis (depending on institution). Auto-match card products. Calculate real missed rewards across your entire spending history.

Browser Extension Platform

Checkout detection on any website. Content script injection with overlay UI. Background sync with 24-hour merchant refresh.

AI Explanation Engine

GPT-4o-mini generates conversational, goal-aware explanations of why each card wins — building user trust and engagement.

Enterprise-grade security for fintech-grade trust

Zero Card Data Exposure

We NEVER store full card numbers or CVVs. Only last 4 digits are retained. No payment processing, no fund custody.

Rate Limiting & Brute Force Protection

Auth endpoints throttled to 10 req/15min. Forgot-password limited to 5 req/hr. Automatic lockout with retry-after headers.

Token Revocation & Session Security

HMAC-SHA256 signed tokens with versioning. Password reset automatically invalidates all existing sessions across devices.

Full Audit Trail

Every login, failed attempt, password reset, data export, and account deletion is logged with IP address and user agent for compliance.

Security Headers & HSTS

X-Frame-Options, CSP, XSS protection, strict referrer policy, and HSTS enforcement in production. Defense-in-depth architecture.

GDPR & CCPA/CPRA Compliant

Full data export, one-click account deletion, 15-section privacy policy, and 28-section terms of service. Built for regulatory readiness.

Comprehensive Legal Documentation

Production-ready legal suite: 15-section privacy policy (GDPR/CCPA/CPRA), 28-section terms of service, information security policy, and creator program agreement with digital signatures. Last updated: April 2026.

Product-led growth with viral mechanics

App Store & Chrome Web Store Launch

Organic discovery through App Store Optimization. The "missed rewards calculator" drives installs — users are shocked by how much they've left behind.

Social Engagement Engine (Twitter/X)

Automated monitoring for credit card rewards conversations across Twitter/X. AI identifies high-intent discussions, drafts contextual replies, and admin reviews before posting — building organic community presence at scale with zero ad spend.

Blog & SEO Content Strategy

Owned content at superpayrewards.com/blog targeting credit card optimization, rewards maximization, and personal finance queries. Long-tail SEO drives organic acquisition with zero marginal cost per visitor.

Affiliate Revenue Loop

Users who discover they need a better card for dining → SuperPay recommends the right one → earns referral revenue. Acquisition cost: $0.

Viral Loops

Every SuperPay interaction creates sharing potential:

• "I saved $47 this month by using the right card" — shareable result

• "I've been losing $1,500–$5,000+/year" — shocking missed rewards stat

• Browser extension visible at checkout — word-of-mouth

• Referral program: give a friend Pro for 1 month

Target Users

• Multi-card holders (3+ credit cards)

• Points & miles enthusiasts

• Credit-building millennials/Gen Z

• Online shoppers (power users of 5+ retailers)

• Personal finance-conscious consumers

Creator-powered growth engine

Fully automated creator affiliate infrastructure — built and live.

For Creators

Everything a creator needs to earn — no friction, no guesswork.

✓ Application portal with automated review

✓ Legally binding digital agreement signing

✓ Personal dashboard with real-time stats

✓ Unique referral links & tracking codes

✓ Pre-written social copy & share tools

For SuperPay

Full-stack admin infrastructure — zero operational overhead.

✓ Admin management dashboard

✓ Automated referral attribution

✓ RevenueCat webhook integration

✓ Commission calculation engine

✓ Payout management system

Why It Matters

Aligned incentives — Creators earn more when users stay subscribed long-term

Unit economics — Creator-driven users have zero customer acquisition cost

Infinitely scalable — Infrastructure handles unlimited creators with no ops overhead

Legal protection — Binding agreements, fraud prevention clauses, arbitration

Most startups promise creator programs. We built the entire infrastructure.

Operator-first founder building long-term infrastructure

Yuri Moreira

Founder & CEO

Operator and consumer product builder. Built SuperPay end-to-end as a solo founder. Long-time observer of the credit rewards market and the gap between what cards offer and what consumers actually capture.

Vision: Build the transaction intelligence layer that sits between every consumer and every payment network.

Approach: Disciplined execution. Infrastructure-level thinking. Long-term category ownership.

Hiring Plan (Lean Infrastructure Mode)

• CTO — Technical co-founder

• 1 Full-stack Engineer — Product & infrastructure

• 1 Growth Lead — Acquisition & conversion

• 1 Security/Compliance Hybrid — Regulatory & security

4-person team. Enough to maintain product, build routing beta, run affiliate loops, and stay compliant.

Advisory Board

Building advisory board across payments industry, fintech, AI, and growth specializations. Targeting fintech angels, founder-operators, micro-VCs, and strategic card ecosystem players.

Raising to scale intelligence

Use of Funds — $3.5M Base (~28-Month Runway)

Disciplined, lean deployment. Target burn: ~$122K/month (Payroll: $73K · Infra/SaaS: $29K · Marketing: $20K). Runway: ~28 months. Path to profitability at 150K users.

Routing intelligence

Card issuing integration

Conversion optimization

Channel partnerships

Network provisioning

Interchange agreements

Regulatory framework

Risk architecture

to support scale

With $5M, we accelerate:

18-Month Targets (Must Be Aggressive)

This round must unlock:

If we don't aim here, Series A gets harder.

What this round unlocks

18-month execution plan to Series A readiness.

Product

• AI reward optimization engine refinement

• PRO+ Outcome Engine & AI Roadmaps

• Real-time routing logic

• SuperPay Digital Card beta

• Automated card benefit matching

Growth

• 250K users

• 8% Pro conversion

• Optimized CAC/LTV model

Infrastructure

• Issuer partnership secured

• Card provisioning live

• Fraud & compliance architecture built

Financial Target

• $5M+ ARR

• $250M+ annual routed volume

Clear milestone → Series A ready.

Lean but Aggressive Team

CEO · CTO · 1 Full-stack Engineer · 1 Growth Lead · 1 Security/Compliance Hybrid

Target burn: ~$122K/month · ~28 months runway · Path to profitability at 150K users

Recommend. Route. Power every transaction.

SuperPay's three-phase roadmap: today we tell you which card to use. Tomorrow we execute it for you. Eventually, we power every transaction autonomously.

The AI Decision Engine

We tell you exactly which card to use — before every purchase. 316-card proprietary database (12,000+ accessible via Plaid across 12K+ banks), Google Places for millions of merchant locations, checkout detection via browser extension, and PRO+ Rewards Roadmap Engine v2 with goal-based strategy, smart new card recommendations, welcome bonus acceleration, and adaptive progress tracking. We optimize before the transaction — not after.

SuperPay Digital Card

A virtual card linked to all your credit cards. We don't just recommend — we route. Every online transaction is intelligently directed to the optimal card in real time. Just pay with SuperPay, and we execute the optimization automatically.

SuperPay Physical Card

A physical card for in-store purchases. Tap or swipe your SuperPay card at any terminal — the AI powers the transaction behind the scenes, routing it to your best card automatically. One card in your wallet that's smarter than all of them combined. Today we recommend. Tomorrow we route. Eventually, we power every transaction.

One card. Every reward. Automatic.

The SuperPay Card auto-routes every transaction to your optimal card — no decisions, no missed rewards, just intelligence.

Today we recommend.

Tomorrow we route.

Eventually, we power every transaction.

SuperPay is the intelligence layer that decides which card you should use before every purchase — and soon, executes it for you. No one should ever use the wrong card again.

Let's build the future of payments together

Get In TouchThis document is confidential and intended solely for the recipient. © 2026 SuperPay Ai, Inc. All rights reserved. Delaware Corporation.